2025/11/25 | Julia Passabom & Mariana Ramirez

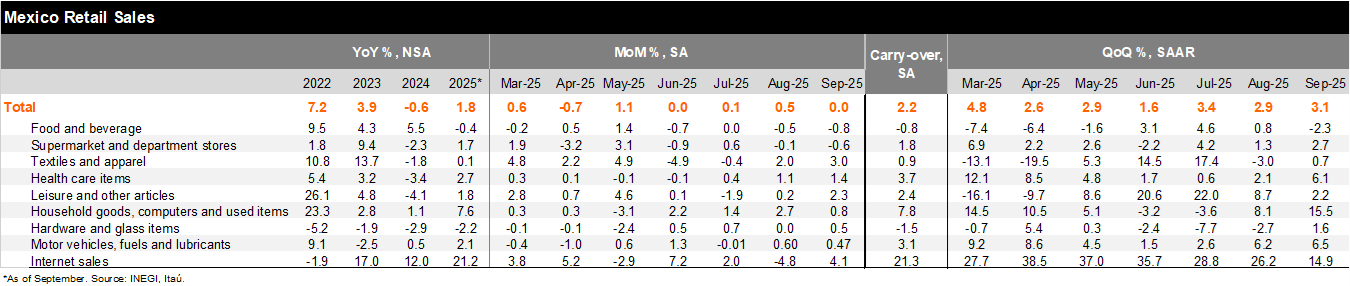

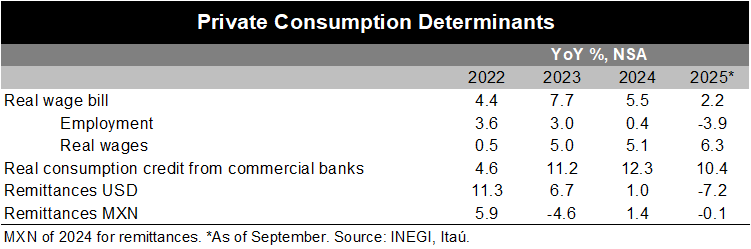

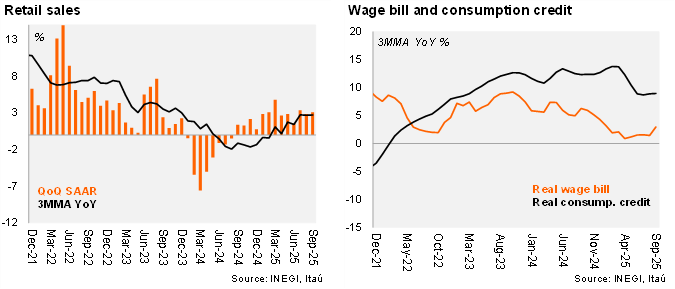

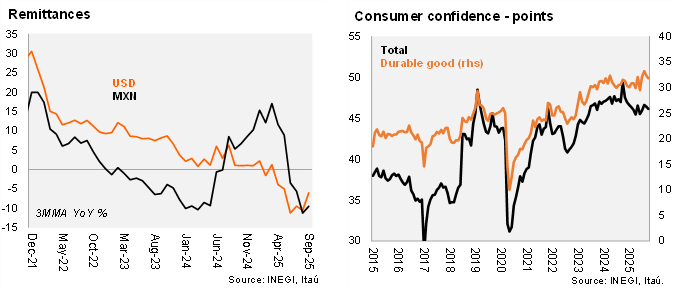

According to a survey of commercial companies, real retail sales rose by 3.3% YoY in September, above Bloomberg’s consensus of 2.2%. On a seasonally adjusted basis, real retail sales remained unchanged sequentially, surpassing the consensus expectation of a 0.4% contraction. Seven out of nine subsectors rose sequentially in September, with textiles and apparel up by 3.0%, health care items by 1.4%, and leisure by 2.3%. However, food and beverages, and supermarkets experienced contractions of -0.8%, and -0.6% MoM, respectively. We continue to identify positive factors for consumption, despite a slowdown compared to the beginning of the year. The real wage bill rose by 2.2% YoY, while real consumption credit from commercial banks increased by 10.4%.

Our take: This data comes from a survey that identifies revenues from companies, which explains the difference from IGAE’s figures that consider value added. Today’s results have a positive bias, with the QoQ/SAAR at 3.1% (up from +2.9% in the previous quarter) and a statistical carry-over of +2.2% for the year. Due to resilient consumption determinants, such as the growing real wage bill and historically high consumer confidence, we anticipate the sector will remain slightly positive in the remainder of 2025. Additionally, we expect private consumption and net exports to be the main drivers of GDP growth this year. While we maintain our GDP forecast of an expansion of 0.6% in 2025, it is somewhat skewed to the downside due to overall worse than expected activity data on 3Q25.

See details below