2025/10/30 | Julia Passabom & Mariana Ramirez

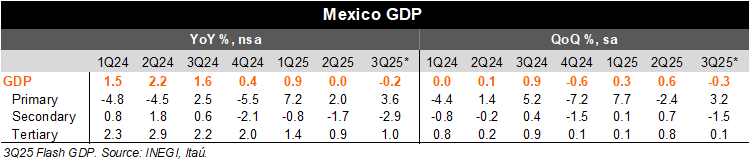

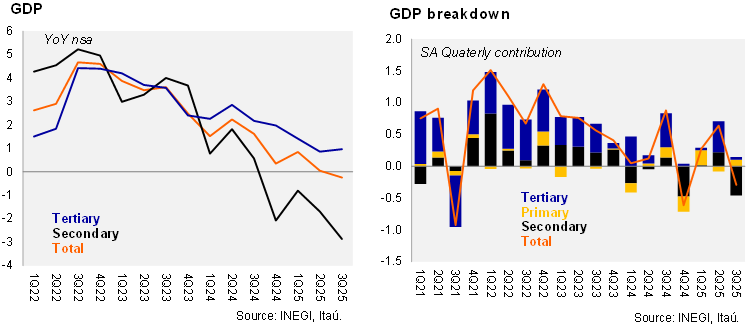

The 3Q25 flash GDP fell by 0.2% YoY, slightly better than Bloomberg’s market consensus and our forecast, both of which were at -0.3% YoY. On an annual basis, primary activities increased by 3.6%, industry declined by 2.9%, and services grew by 1.0%. As of 3Q25, GDP rose by 0.2% due to growth in primary and tertiary activities, with the industry being the main drag. Using seasonally adjusted figures, GDP contracted by 0.3% QoQ (Bloomberg -0.4%, Itaú -0.2%) due to the industry's performance at -1.5%, despite increases in both services (+0.1%) and agriculture (+3.2%). With these seasonally adjusted results, GDP grew by 0.5% annually in the first nine months of the year.

Considering that the observed monthly GDP averaged a contraction of 1.0% YoY in July-August, today’s estimate implies that September was close to 1.6% YoY. Our calculations suggest a 0.1% monthly growth (down from +0.6% in August), which is in line with INEGI’s nowcast. The final GDP release is scheduled for November 21.

Our take: Today’s release suggests that activity expectedly decelerated in the second half of the year, with a statistical carry-over for 2025 at 0.6%. This behavior was already anticipated, after a very strong 2Q25. Looking ahead, we expect Mexico’s growth to continue receiving some support from external factors, but these will become less relevant, compared to the beginning of this year. The outlook for domestically driven sectors will remain mixed, with a slowdown in local services and a contraction in investment. However, investment could continue to show signs of improvement, based on the start of public projects, such as railways construction and road maintenance. We maintain our GDP forecast of an expansion of 0.6% in 2025.

See detailed data below