2025/09/08 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

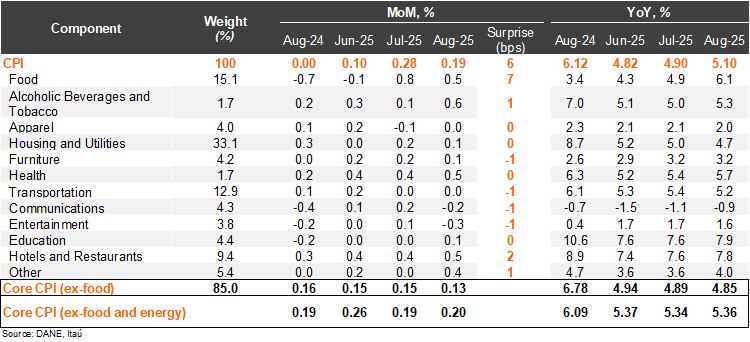

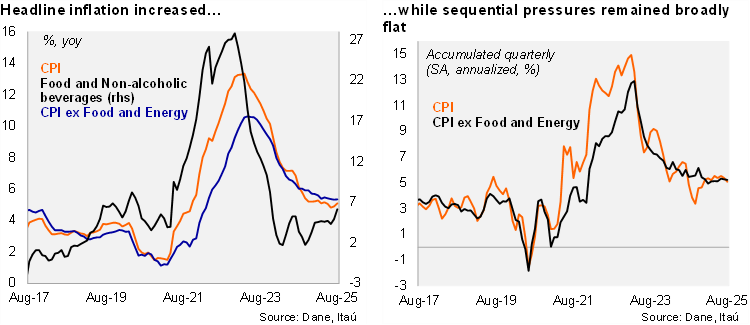

Inflation rose above 5% in August, resulting in a second-month sequence of rising annual prints. Consumer prices rose by 0.19% MoM in August, slightly below the Bloomberg market consensus of 0.21%, while above our 0.13% call. The main positive contributors in the month were food prices (+0.45%; +8bps), hotels and restaurants (+0.49%; 6bps) and housing and utilities (+0.06%; +2bps), with food away from home being the item with the largest contribution to the monthly print. Food prices explained most of the upside surprise relative to our forecast. Consumer prices excluding food rose by 0.13% MoM (+0.16% one year earlier), while inflation excluding food and energy rose by 0.20% MoM (+0.19% one year ago). On an annual basis, headline inflation increased by 20bps from July to August (5.1%), while core inflation rose by 2bps to 5.36%. Cumulative inflation in the year through August rose to 4.16% (4.26% in 2024), already clearly above the ceiling of the tolerance range in the central bank’s 3% target.

Services inflation remains elevated. Non-durable good inflation (mainly food) came in at 4.13% YoY, increasing by 59bps from the previous month. Meanwhile, energy inflation dropped 52bps to 0.61% YoY, amid a negative contribution from electricity prices (-6bps, -1.61% MoM). Durable goods rose by 15bps from the previous month to 0.14%, returning to positive territory for the first time since January 2024. Services inflation dropped by 7bps to 6.43% (9.51% peak in September 2023), partly due to lower indexation pressures from rent prices (5bps, 0.26% MoM). At the margin, we estimate that inflation accumulated in the quarter reached 5.1% (SA, annualized; +5.5% in 2Q25). Core inflation remains elevated at 5.2%, from 5.3% in the 2Q25 (SA, annualized).

Our take: Our preliminary estimate for September’s monthly inflation, scheduled for release on October 7, ranges between 0.2% and 0.3%, leading the CPI annual print to remain broadly unchanged. In the second half of the year, base effects and rising gas prices are expected to challenge the disinflation process. As a result, the bar remains high for any near-term cuts to the monetary policy rate. We anticipate the rate will hold steady at 9.25% throughout this year, with a projected decline to 8.25% by the end of 2026.