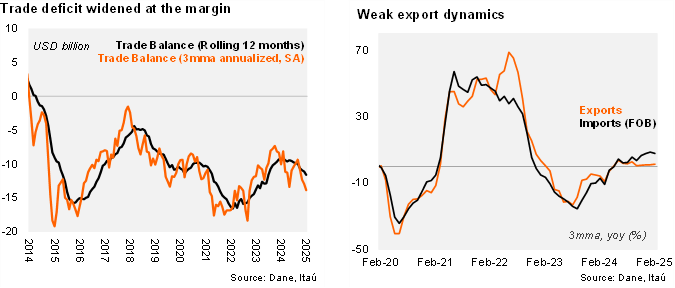

The trade deficit In February came in at USD 1.2 billion, widening by USD 0.5 billion with respect to February 2024. The trade deficit was broadly in line with both the Bloomberg market consensus and our call (USD 1.3 billion). Total imports (FOB) rose by 9.8% yoy (+7.4% in January), boosted by fuels, agricultural and manufacturing imports. Meanwhile, exports fell by 0.8% (+4.3%YoY in January), still dragged by oil and coal exports. As a result, the 12-month rolling trade deficit sits at USD 11.5 billion (USD 10.8 billion in 2024; USD 9.7 billion in 2023).

Imports remain upbeat. The 9.8% yoy increase was boosted by doubling of capital goods for agriculture, fuels (+59%yoy), raw materials for intermediate products and durable consumption goods (+15.8% yoy). In the rolling quarter ending in February, imports increased 7.8% yoy (+7.7% in 4Q24). Imports excluding fuels and transportation equipment rose by close to a double-digit rate from last year. At the margin, we estimate imports continue to grow at around 20% qoq/saar. As of February, imports from the US accounted for 24.6% of the total.

Exports contracted, dragged by commodities. Exports fell by 0.8% yoy (+4.3%YoY in January). While coffee exports continued to post a strong performance, weak oil and coal dynamics explain the overall decline. In the quarter ending February, exports increased 1.3% yoy (0.9% in 4Q24). At the margin, exports fell 2.8% qoq/saar (8.5% in 4Q24). As of February, exports to the US accounted for 28.8% of the total.

Our Take: While commodity prices continue to drag exports, imports dynamics remain strong. We expect a gradual widening of the CAD this year to 2.6% (1.8% of GDP in 2024).