2025/08/29 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

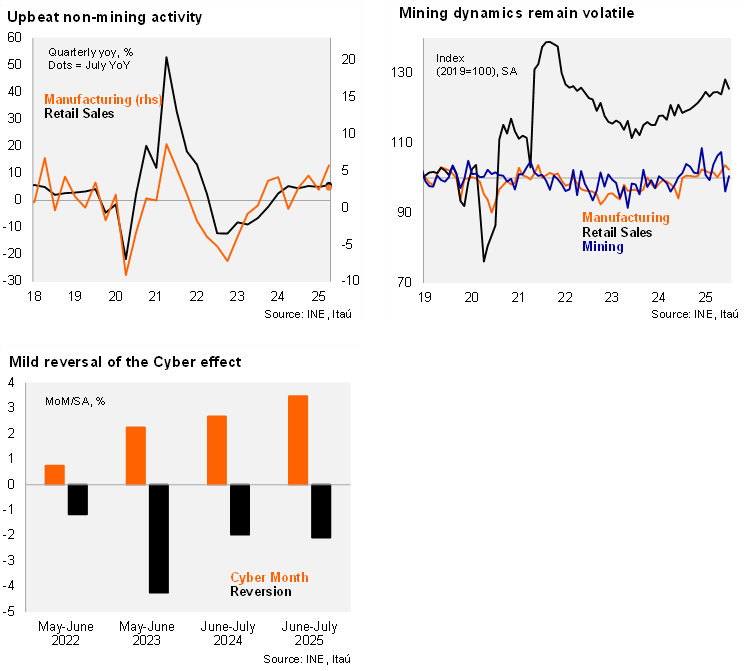

Activity indicators in July came in mixed, with mining particularly underperforming, leading us to expect an annual increase of 1.3% YoY in Monday’s Imacec publication (3% in June). Retails sales increased by 5.7% YoY (6% in June), above the Bloomberg market consensus of 5.5% and our 5.3% call. Sequentially retail sales fell 2.1% MoM/SA, unwinding the Cyber sales effect in June (+3.5% MoM/SA). Manufacturing rose by 2.7% YoY, below both the Bloomberg market consensus and our call of 3.0%, while also posting a sequential decline (-1,2% MoM/SA). The upside manufacturing pull stems from food processing, while pharmaceutical products and chemicals were significant drags. Mining contracted for a second consecutive month (-0,9% YoY), as ore-grades suffered at a relevant mining company. The weak mining activity follows 4.2% drop in June amid closure of a mining plant for maintenance. The tragedy at El Teniente mine in August will keep mining dynamics downbeat. Overall, industrial production posted 1.0% YoY increase (3.2% in June).

While activity data has been volatile, non-mining momentum is favorable. Retail sales rose by 5.8% QoQ/saar in the rolling quarter ending in July, after the 4.6% in 2Q25 and 8.5% in 1Q24. Manufacturing rose 6.4% QoQ/saar (+0.8% in 2Q25). Mining contracted by 6.9% QoQ/saar (7.9% in 2Q25).

Our take: Excluding the volatile mining component, activity dynamics remain upbeat. Growth this year will be supported by resilient private consumption amid elevated real wage growth, along with the mining-led investment recovery. Supply shocks to mining place a downward bias to our 2.6% growth call for the year.