2025/08/29 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

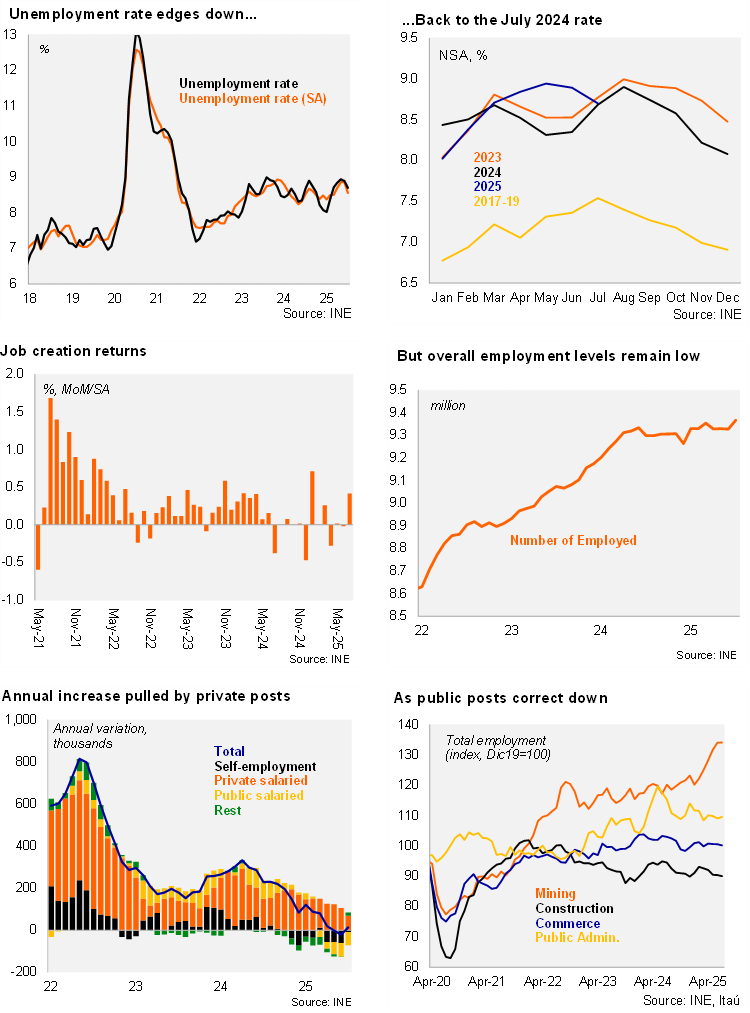

The unemployment rate reached 8.7% in July quarter, in line with same month last year. Over the prior rolling-quarter, the unemployment rate had been, on average, 0.5pp higher over one year. The Bloomberg market consensus and our call was 9.1%. Employment rose 0.8% YoY (+73 thousand posts; 0% in June), while the labor force increased 0.8% (0.6% in June). On a seasonally adjusted basis (SA), employment growth was 0.4% from the June quarter, the first significant increase since March. Despite the retreat, the unemployment rate (SA) has hovered at or above the upper bound of the BCCh’s estimated NAIRU (7-5-8.5%) for more than a year. Labor market informality remained at 26%, down 0.4pp over one year. Manufacturing and Mining were key job creating sectors over twelve months, while construction and retail retreated. The annual employment change continues to show an offset between positive formal job creation (+88 thousand), lifted by the private sector while public posts adjust, and a decline in informal posts (-15 thousand).

Our Take: Despite the surprise of this month, overall data is in line with slack in the labor market, in the context of substantial increases in labor costs over the past few years. While non-mining activity consolidates its growth recovery, the pull is derived from the external backdrop, mining investment, elevated real wage growth and transitory boosts from tourism and frontloading of fiscal spending. We expect an average unemployment rate of 8.7% this year. Still weak commercial loan dynamics, growing labor market slack amid anchored inflation expectations consolidate the central bank’s scenario of lower the policy rate over the upcoming quarters. Yet the uptick in core inflation in recent months leads us to expect a pause in September. We see the policy rate ending the year at 4.5%