2025/09/01 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

While fiscal consolidation continued in July, a welcome development, nominal and structural deficits are likely to come in above official forecasts.

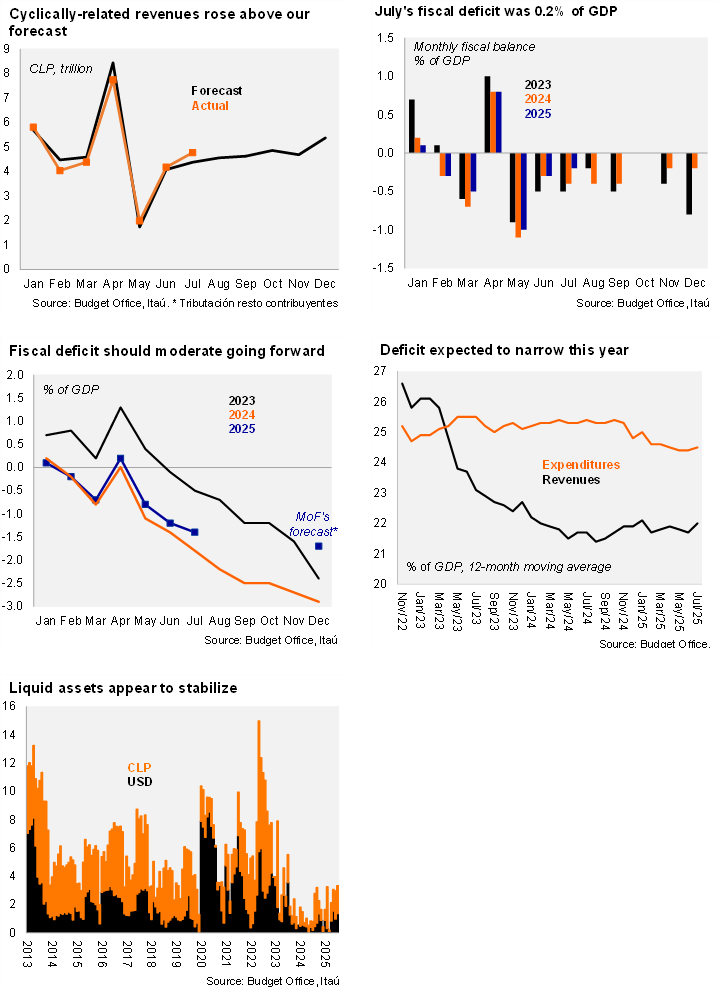

The Central Government’s real revenues jumped by 19.4% YoY in July, with broad-based improvements. Cyclically-related real revenues (tributación resto contribuyentes, comprising roughly 80% of total revenues) spiked, rising by 19.4% YoY, breaking a string of annual contractions likely related to tax season noise; these revenues in July were above our forecast, almost compensating for earlier misses in the year (see chart). Mining-related revenue from Codelco outperformed, linked to a dividend payment in the month. Even though private mining revenue contracted on an annual basis in July, these revenues in the year are up by 74% YoY, reflecting the first full-year of the new mining royalty law, elevated copper prices, and greater copper production. Total real revenues accumulated in the year through July have increased by 6.3% YoY (4.3% in June), inching up towards the MoF’s annual 7.6% forecast (does not consider greater revenues from “corrective measures”, which mostly rely on legislative approval).

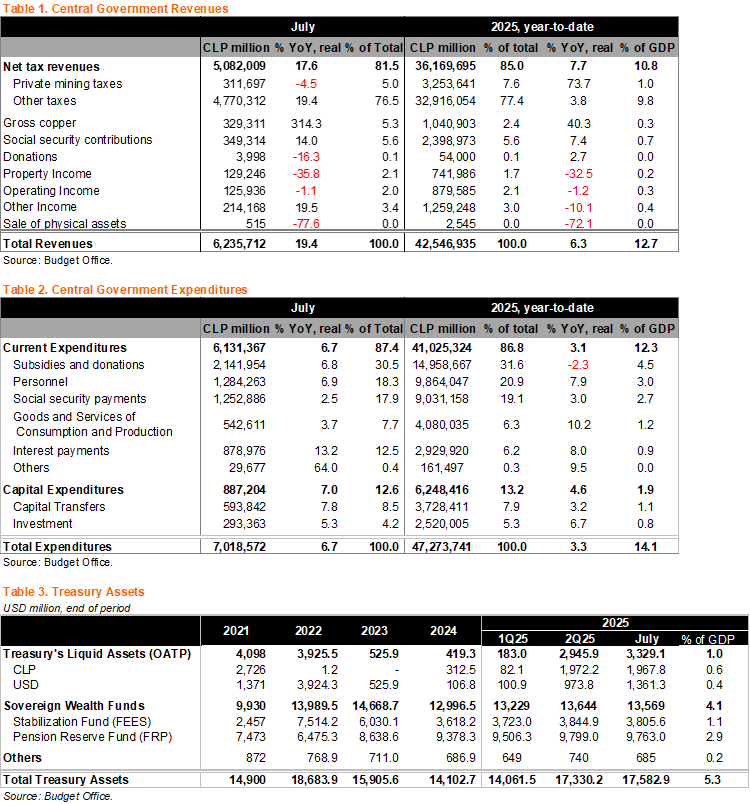

Real spending rose by 6.7% YoY in July. Current expenditure increased by 6.7%, with increments across all components, taking the year-to-date rise to 3.1% and accumulating 59.1% of the annual budget, similar to 2024 (58.7%). Capital expenditure also edged up in July by 7.0% YoY, leading to a cumulative rise in the year of 4.6%, taking this component’s expenditure to 47.7% of the annual budget, slightly above last year’s progress at the time (47.2%). We believe that after frontloading in the first half of the year, capital spending is likely to slow. Total spending in the year through July has increased by 3.3%, still above the 2.2% official forecast.

July’s monthly fiscal balance reached -0.2% of GDP, a smaller deficit than last year (July 2024 at -0.4%) same as June 2024. The cumulative fiscal balance through July fell to a deficit of 1.4% of GDP, a smaller deficit than the 1.8% through July in 2024.

The 12-month rolling fiscal deficit fell to 2.5% of GDP, from 2.7% of GDP in June. On a 12-month moving average basis as of the end of July, the central government’s revenues rose to 22.0% of GDP, and expenditures 24.5%, leading to a nominal deficit of 2.5%, improving from 3.7% of GDP a year earlier. We expect a gradual narrowing of the deficit, primarily due to an improvement in revenues.

Liquid assets at the Treasury were essentially flat sequentially in June. Liquid assets in the Treasury rose again at the margin to USD3.3 billion in July (from USD2.9 billion in June), well above July 2024’s level (USD795 million). As we have mentioned in previous reports, cash buffers are improving, a welcome development, driven by debt issuance and greater revenues. AUM in the sovereign wealth funds were little changed, likely reflecting valuation effects. The Stabilization Fund (FEES) was flat at USD3.8 billion, and the Pension Reserve Fund (FRP) also unchanged at USD9.8 billion. The MoF already reported a USD200 million withdrawal from the FRP during August to finance a loan to the social security fund, as part of the implementation of the pension reform.

Our take:

• Revenue improvements are taking place in line with our view for the fiscal accounts, leading us to be more constructive than consensus. Spending is still running at an above-forecast pace and will have to be reined in further, posing challenges in an election year. Our 2025 nominal deficit forecast of 2.0% of GDP implies a deficit of 0.6% of GDP for the August-December period, well below the 1.2% of last year during the same period.

• Following last year’s large fiscal miss, with the structural deficit target reaching 3.3% of GDP, significantly above the 2024 official target of 1.9% of GDP, the MoF has revised its structural deficit forecast up in each of the last macro-fiscal forecasts from the official 2025 target of 1.1% of GDP to 1.6% in February and 1.8% in July.

• In its recent quarterly report, the Autonomous Fiscal Council reiterated the stress on the fiscal accounts and called for additional measures to contain spending growth. We believe the next administration will have to implement structural expenditure cuts for at least 0.5% of GDP in 2026 to ensure a swifter fiscal consolidation and the stabilization of gross public debt below the 45% of GDP threshold.

• On the financing front: Even though cash levels have continued to improve, we believe that the MoF will continue with its USD16 billion annual gross debt issuance plan, issuing up to USD2.5 billion in local currency short-term notes by year-end (likely prior to the November 16 election).

• On policy and reforms: The revenue-neutral tax reform – according to official estimates – presented by the administration in July is likely to face resistance in Congress as elections loom in November and the 2026 budget discussions begin in October. Measures that enhance this year’s revenues – so called corrective measures – remain in discussion in Congress.

• Upcoming data: The Budget Office will release August’s fiscal by the end of September, in tandem with presentation of the 2026 budget bill. The 3Q25 Public Finance Report is scheduled for October 1.