2025/11/28 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

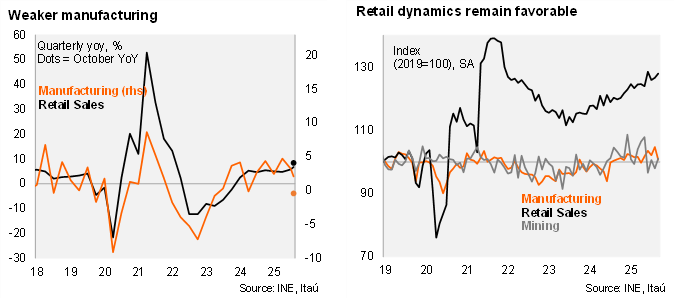

According to the National Statistics Institute (INE), real retail sales rose 8.4% YoY (6.5% in September), well above Bloomberg’s market consensus of 5.4%, and our call of 6.2%. Electronics and household technology (17.4% YoY), apparel and footwear (14.3%) and food (5.1%), with the boost at least partly stemming from cyber sales events during the month (split between September and October during 2024). Sequentially, retail sales rose 1.4% MoM/SA, building on the 1.1% increase in September. Meanwhile, manufacturing output fell 0.4% YoY, below market expectations of +0.9% (Itaú: +0.5%), mainly due to declines in paper manufacturing (-9.4%), pulp production (-8.7%) and machinery and equipment (-17%). Sequentially, manufacturing contracted 0.7% (-3.8% in September). Mining production remained weak (-0.8% YoY), driven by lower ore grades and reduced mineral processing. Mining levels were essentially flat at the margin. Annually, mining has contracted for the past five months. As a result, industrial production declined 0.4% over twelve months, falling 0.3% MoM/SA (-0.5% in September). We expect October Imacec to grow 1.7% YoY (to be released on Monday; 2.7% in September), with non-mining activity a tick above 2%.

Retail retains strong momentum, while mining lags behind. Retail sales rose by 6.4% QoQ/saar in the quarter ending in October (3.7% in 3Q), while manufacturing decreased 2.3% QoQ/saar (+3.5% in 3Q25). Mining contracted by 6.3% QoQ/saar (-13.7% in 3Q).

Our take: October’s sectoral data continues to signal strong consumption momentum, supported by real wage gains, easing inflation, and lower borrowing rates, underpinning private consumption as a key driver of growth this year. However, persistent challenges in the mining sector pose risks to our 2025 growth forecast of 2.5%. With non-mining activity maintaining a solid performance and investment prospects improving, the Central Bank will likely revise its 2026 GDP growth forecast up at the December IPoM (currently 1.75-2.75%). On the other hand, inflation pressures have come in softer than expected by the BCCh. We expect a 25bp rate cut to 4.5% in December.