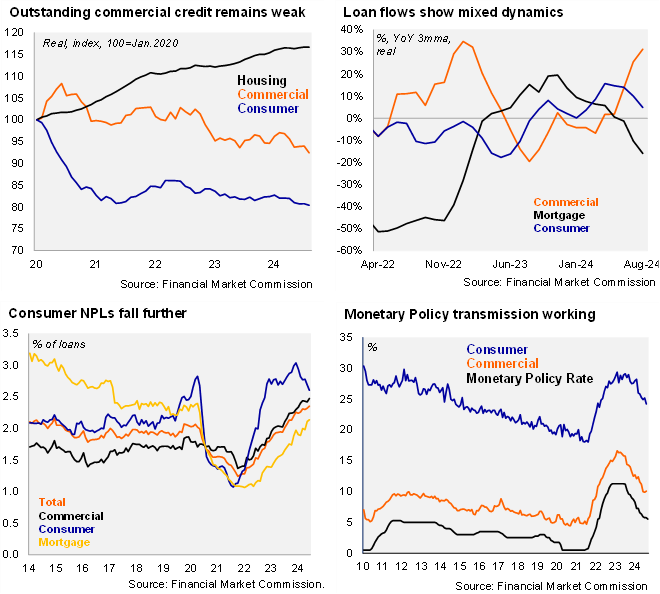

According to the Financial Market Commission, the banking system’s stock of outstanding real loans in Chile fell in August by 2.04% YoY, after declining by 0.56% YoY in July (-2.8% in August 2023). Outstanding real commercial loans in Chile plummeted in August falling by 4.45% YoY, (-2.99% in July, -5.87% in August 2023), declining on an annual basis since May 2022. Even though the stock of outstanding real commercial loans fell again, on a flow basis they rose by 31.2% in the quarter ending in August, the fastest annual pace since February 2023, likely reflecting base effects. Outstanding consumer loans in Chile slipped and resumed a downward trend after months of improvement, declining by 2.01% in August (-0.95% in July, -1.93% in August 2023), contracting on an annual basis since January 2023. Real outstanding mortgage loans in Chile rose by 2.09% YoY (2.27% in July, 2.01% in August 2023).

Non-performing loans (defined as delinquencies of more than 90 days) rose slightly at the margin to 2.35% (2.32% in July, 1.94% in August 2023), in line with our expectation for a stabilization at the highest levels since 2014. As such, the banking system’s NPLs remain well above the March 2014 – March 2020 average of 1.95%. By loan type, consumer NPLs fell at the margin to 2.61% (2.69% in July, 2.7% in August 2023), resuming a gradual downward trend that had been interrupted with a marginal increase in June; consumer NPLs peaked in the cycle at 3.04% in February, with the improvement likely linked to lower borrowing costs and improvements in the real wage bill. Mortgage NPLs continue to rise, reaching 2.14% in August, well above the 1.59% of August 2023 (2.11% in July 2024), yet still well below the pre-covid 2.4% level. Commercial NPLs also rose at the margin to 2.47% (2.42% in July, 2.02% in August 2023), close to the highest level at least since 2014, trending up from the low of 1.37% in December 2021.

Borrowing rates for commercial loans rose slightly in August but should continue to fall in the coming months. Interest rates in nominal terms on consumer loans averaged 24.22% in August, down from 25.18% in July yet below the 28.48% of August 2023; the spread with respect to the monetary policy rate reached 18.47pp, slightly above the two-year average (18.1%). In contrast, interest rates in nominal terms on commercial loans rose slightly in August, averaging 10.06%, up from 9.88% in July, and well below the 14.39% of August 2023; the spread with respect to the monetary policy rate fell rose to 4.31%, below the two-year average (4.5%). Borrowing rates for consumer and commercial loans are likely to trend down further, considering the BCCh’s updated guidance and historical spreads. Inflation-linked rates on mortgages fell in August to 4.97%, interrupting three months of consecutive gradual increases yet remaining well above the 4.22% of August 2023.

Our take: Weak commercial loan dynamics are still a source of concern. Credit dynamics have been at the forefront of the monetary policy discussion in Chile, especially considering the relevance that commercial loans may signal for the recovery of investment. August data suggests commercial loan dynamics have yet to turn the corner. Following the BCCh’s guidance, borrowing costs for consumer and commercial loans should continue to gradually decline. The fall in consumer NPLs is in line with our view, yet the persistent rise in mortgage NPLs should be monitored which may be linked to mortgages that shifted from fixed to variable rates. The Financial Market Commission will release data for September on October 31.