According to the Financial Market Commission, the banking system’s stock of outstanding real loans in Chile fell again in June, declining by 0.78% YoY (0.0% in June 2024). Outstanding real commercial loans in Chile contracted by 2.47% in June (-1.69% in June 2024), declining on an annual basis since May 2022. Outstanding consumer loans in Chile, in contrast, rose on an annual basis again, increasing by 1.41% YoY (-1.37% in June 2024). The stock of real outstanding mortgage loans in Chile continues to gradually decelerate, rising by 1.07% YoY in June (2.37% in June 2024).

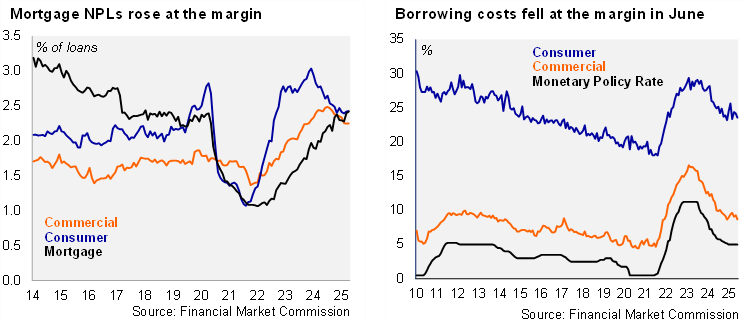

Non-performing loans (defined as delinquencies of more than 90 days) remained flat at 2.31% in June, in line with last year’s levels. The banking system’s NPLs still remain well above the March 2014 – March 2020 average of 1.95%. By loan type, consumer NPLs rose slightly at the margin for the second consecutive month to 2.43% in June, from 2.42% in May (2.78% in June 2024), down from the cycle peak of 3.04% in February 2024. Mortgage NPLs continue to rise, reaching 2.42% in June (1.98% in June 2024). Commercial NPLs have been essentially flat for the last three months roughly at 2.25%, down from last year’s levels (2.43% in June 2024).

Bank lending rates fell in June. According to the BCCh, interest rates in nominal terms on commercial loans fell at the margin in June to an average of 8.66, from 9.28% in May, approaching the lowest level in several years; the spread with respect to the monetary policy rate fell to 3.66pp, well below the two-year average of 4.3%. Separately, interest rates in nominal terms on consumer loans averaged 23.55% in June, down from 24.19% in May; the spread with respect to the monetary policy rate fell to 18.55pp, somewhat below the two-year average of 19%. Inflation-linked rates on mortgages were essentially unchanged for the third consecutive month at 4.39%.

Our take: Weak commercial credit dynamics suggest non-mining investment is unlikely to pick up in the short term. Persistent slack in the labor market is likely to weigh on NPLs; the rise in mortgage NPLs, already back to pre-Covid levels, is a key watchpoint. Borrowing costs may gradually decline going forward, considering the recent 25bp cut by the BCCh this month, and additional cuts priced in for the rest of the year. Pressure on rates at the long end, stemming from global factors, should weigh on mortgage rates and hence demand. The Financial Market Commission will release bank credit data for July by the end of August.