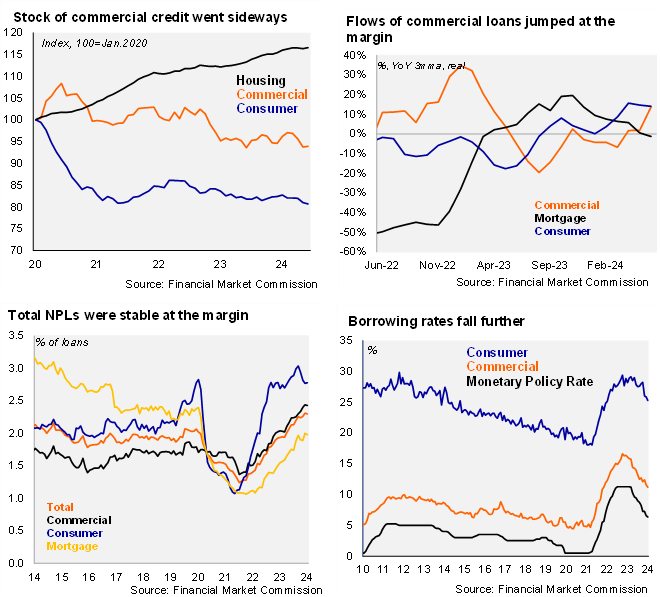

According to the Financial Market Commission, the banking system’s stock of outstanding loans in Chile were flat in real terms in June, after two consecutive months of annual contractions (-1.15% in May; -4.8% in June 2023). Outstanding real commercial loans in Chile fell again, contracting by 1.69% YoY in June (-3.4% in May; -8.53% in June 2023), declining on an annual basis since May 2022. Even though the stock of outstanding real commercial loans fell again, on a flow basis they rose by 13.1% in 2Q24, the fastest annual pace since March 2023, likely reflecting base effects, with loan flows essentially back to 2023 levels. Outstanding consumer loans in Chile declined by 1.37% YoY (-1.86% in May, -3.83% in June 2023), contracting on an annual basis since January 2023. Real outstanding mortgage loans in Chile rose by 2.37% YoY, essentially unchanged from the previous months (2.5% in May, 1.73% in June 2023).

Non-performing loans (defined as delinquencies of more than 90 days) were essentially flat at the margin at 2.30% in June (2.31% in May, 1.94% in June 2023), in line with our expectation for a stabilization at the highest levels since 2014. As such, the banking system’s NPLs remain well above the March 2014 – March 2020 average of 1.95%. By loan type, consumer NPLs were essentially flat in June at 2.78% (2.77% in May, 2.69% in June 2023), interrupting a string of sequential improvements from the cycle peak of 3.04% reached in February. Notwithstanding the marginal rise, the improvement in consumer NPLs over the past several months appears consistent with lower borrowing costs, and improvements in the real wage bill, and among other factors. Mortgage NPLs fell slightly to 1.98% (2.0% in May, 1.55% in June 2023), yet still well below the pre-covid 2.4% level. Commercial NPLs fell slightly to 2.43% in June (2.44% in May, 2.04% in June 2023), close to the highest level at least since 2014, trending up from the low of 1.37% in December 2021.

Monetary policy transmission working smoothly as borrowing rates fell further in June. Interest rates in nominal terms on consumer loans averaged 24.91% in June, down slightly from 25.27% in May, and the 28.91% of June 2023; the spread with respect to the monetary policy rate reached 19pp, slightly above the two-year average (18.1pp). Similarly, interest rates in nominal terms on commercial loans averaged 9.97% in June, down from 11.18% in May, well below the 15.8% of June 2023; the spread with respect to the monetary policy rate fell to 4.06pp, below the two-year average (4.5pp). The decline in interest rates on commercial and consumer loans is likely to slow for consumer loans and pause for commercial loans, considering the BCCh’s guidance on rates and historical spreads. In contrast to the declines in shorter term loans, inflation-linked rates on mortgages rose to an average of 5.0% in June, up slightly from 4.97% in May, and substantially above the 4.2% of June 2023.

Our take: Even though the rise in commercial loan flows in June are an unexpected welcome surprise, we maintain a cautious view on credit dynamics. The BCCh’s 2Q24 Bank Lending Survey, published earlier this month, suggested that credit supply remained stable, while demand weakened at the margin, especially from large firms. The steep decline in consumer and commercial interest rates is likely to slow as we expect the BCCh to take the monetary policy rate to 5.5% and then pause for a prolonged period. Importantly, June brought greater evidence of our view of a stabilization in overall NPLs. The Financial Market Commission will release data for July on August 30.