2025/11/28 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

According to the Financial Market Commission, the banking system’s stock of outstanding real loans in Chile fell annually by 0.37% in October (-1.62% in Oct-24), contracting after two consecutive annual expansions on an annual basis. Outstanding real commercial loans in Chile slipped back to negative territory in October, declining by 1.99% (-4.7% in Oct-24). In contrast, outstanding real consumer loans in Chile rose by 2.56%YoY (-1.15% in Oct-24), while mortgage loans in Chile increased by 1.43% YoY (1.73% in Oct-24).

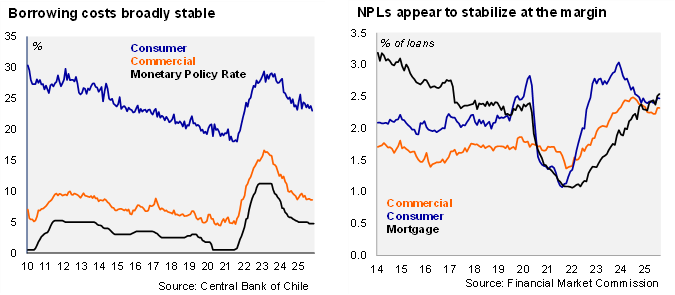

Commercial bank lending rates were stable in October. According to the BCCh, average nominal rates on commercial loans were sequentially unchanged at 8.6% in October, remaining at the lowest since November 2021; the spread with respect to the monetary policy rate remained at 3.85pp, below the two-year average (4.2pp). Nominal rates on consumer loans averaged 23.01% in October, from 23.8% in September; the spread with respect to the monetary policy rate declined to 18.265pp, below the two-year average (19.04pp). We envisage little changes in bank lending rates for commercial and consumer loans in the near term as the BCCh’s cycle of cuts has nearly concluded. Inflation-linked rates on mortgages fell at the margin for the fifth consecutive month to 4.16% in October, from 4.21% in September.

Non-performing loans (defined as delinquencies of more than 90 days) were essentially flat at the margin, at 2.39% in October (2.36% in Oct-24). The banking system’s NPLs still remain above the March 2014 – March 2020 average (1.95%). By loan type, consumer NPLs were flat at 2.47% (2.54% in Oct-24), below the cycle peak of 3.04% in February 2024. Mortgage NPLs rose again to 2.54% (2.23% in Oct-24). Commercial NPLs were unchanged sequentially at 2.32% (2.47% in Oct-24).

Our take: Overall, we maintain our view of a gradual recovery in credit.

The mining-led investment recovery is expected to spill over into non-mining investment dynamics and credit demand. Mortgage loans decelerated despite the transitory government-financed subsidy program. The rise in consumer lending takes place as retail sales continue to surprise positively, albeit along with recovering household confidence.

Room for a significant decline in commercial and consumer borrowing costs is limited considering our view that the Central Bank is near the conclusion of the rate-cutting cycle.

The Financial Market Commission will release bank credit data for November by the end of December.

Finally, October data seems broadly consistent with the BCCh’s characterization of bank credit in the recent Financial Stability Report. The BCCh’s Board only assessed maintaining the CCyB at 0.5% of RWAs in the 2S25 Financial Policy Meeting. Having fully transitioned capital requirements to Basel III by this yearend, the BCCh will assess if macro-financial and credit conditions merit a transition of the CCyB to neutral (1% of RWAs) in May 2026, which implementation would be in at least a year. The next Financial Policy Meeting is scheduled for May 16.