2025/10/29 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

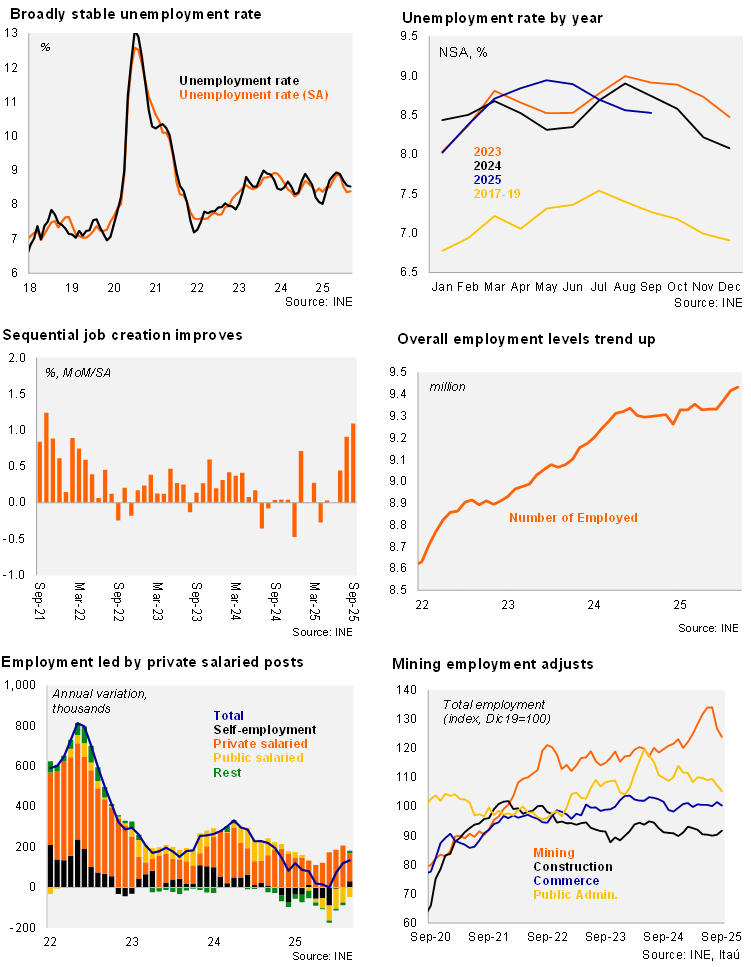

The unemployment rate reached 8.5% in the third quarter of the year, 0.2pp down from 3Q24, while in line with both the Bloomberg consensus and our call. Employment rose 1.5% YoY (0% in 2Q), and the labor force did so by 1.2% (0.6% in 2Q).On a seasonally adjusted basis (SA), employment increased 1.1% from the June quarter (-0.2% QoQ/SA in 2Q). The unemployment rate (SA; 8.4%) is down 0.5pp from the 2Q peak. Nevertheless, the unemployment rate has hovered at or above the upper bound of the BCCh’s estimated NAIRU (7-5-8.5%) for more than a year. Labor market informality sits at 26.2%, down 0.8pp over one year. Informatics, administration services and health were key job creating sectors over twelve months. The annual employment change continues to show an offset between positive formal job creation (+170 thousand YoY), lifted by the private sector (+90 thousand) while public posts adjust and informal posts tick down.

Our Take: In the context of substantial increases in labor costs over the past few years, labor market dynamics had been downbeat but improving non-mining activity and signs of recovering credit demand are likely leading to an inflection in labor demand, albeit still at low levels. We have a downside bias to our average unemployment rate estimate of 8.7% for this year. Looking ahead, if business sentiment recovery consolidates, and the investment dynamism spills over to the construction sector amid property purchasing incentive programs and lower average interest rates, employment dynamics should improve and support a retreat deeper into the BCCh’s NAIRU range. The improving investment outlook and recovering labor market will likely sustain demand-led inflationary pressure, raising the risk that the BCCh keeps rates stable for longer than our baseline scenario of a rate cut in December.