2025/10/08 | Diego Ciongo & Soledad Castagna

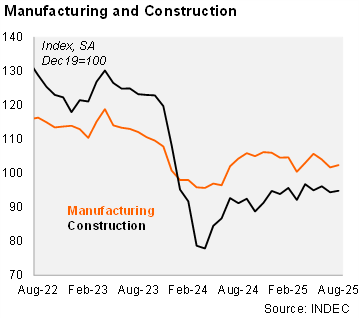

Manufacturing increased sequentially in August. The IPI manufacturing index increased by 0.6% mom/sa in August, after falling by 2.2% in July. However, industry output fell by 0.3% qoq/sa in the quarter ended in August, following a 1.0% expansion in 2Q25. On an annual basis, manufacturing fell by 4.4% in August and increased by 1.0% in the quarter ended in that month. Only one of nine sectors grew on an annual basis in August.

Construction also expanded in August. The construction index rose by 0.5% mom/sa in August, after falling 1.9% in the previous month. Moreover, construction rose by 0.5% qoq/sa in the quarter ended in August (2.2% qoq/sa in 2Q25). Construction activity increased by 0.4% yoy in August and by 4.7% yoy in the quarter ended in that month. Employment in the sector increased by 4.6% relative to July 2024 (figures have a one-month lag). According to a qualitative survey, 64.9% of those involved in private construction expect no changes in activity levels over the next three months. Meanwhile, 7.4% expect an increase and 27.7% anticipate a decline. Among companies primarily engaged in public works, 28.9% anticipate a decrease in activity levels during the next three months, while 60.0% expect no change and 11.1% expect an increase.

Our take: The sequential increases in manufacturing and construction provide a slight relief to activity, although the economy is likely heading to a technical recession. Our 2025 GDP growth forecast stands at 3.8%, primarily due to a high carryover from last year.