2025/10/22 | Diego Ciongo & Soledad Castagna

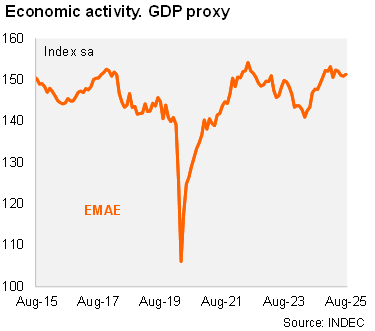

According to the EMAE (official monthly GDP proxy), economic activity rose by 0.3% MoM/SA in August, after three consecutive monthly contractions. Consequently, activity decreased 0.4% in the quarter ended in August after falling 0.1% QoQ/SA in 2Q25. On an annual basis, activity rose by 2.4% in August and by 3.9% in the quarter ended in that month (+6.3% yoy in 2Q25). If the economy were to remain flat at end-August levels, GDP would rise by 3.8% in 2025.

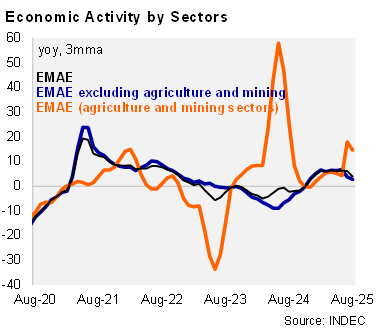

All sectors except manufacturing expanded on an annual basis in the quarter ended in August. Primary activities rose by 14.6% YoY during this period (compared to +4.3% YoY in 2Q25), while Services (including the commerce sector) expanded by 2.7% YoY (vs. 4.9% in 2Q25). Construction rose by 2.2% YoY (from 10.6% YoY in 2Q25) due to a base effect amid the freezing of public works in the same period of 2024. On the other hand, manufacturing fell by 2.3% YoY (vs. a gain of 6.9% YoY in 2Q25).

Our take: Our GDP growth forecast for 2025 stands at 3.8%. Due to the weak performance of leading indicators and the impact of high real interest rates on consumption amid political turmoil, a technical recession in 3Q25 is likely, despite the recent sequential monthly rebound. The GDP proxy for September will be published on November 24.