2025/08/20 | Diego Ciongo & Soledad Castagna

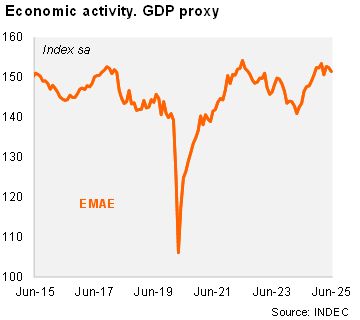

Activity fell sequentially again in June. According to the EMAE (official monthly GDP proxy), economic activity contracted by 0.7% MoM/SA in June, after decreasing 0.2% MoM/SA in May. Consequently, activity remained stable in 2Q25 (0.0% QoQ/SA in 2Q25) after increasing 0.9% QoQ/SA in 1Q25. On an annual basis, activity rose by 6.4% in June and by 6.5% in 2Q25 (+5.8% yoy in 1Q25). The statistical carryover for 2025 stood at 4.2%.

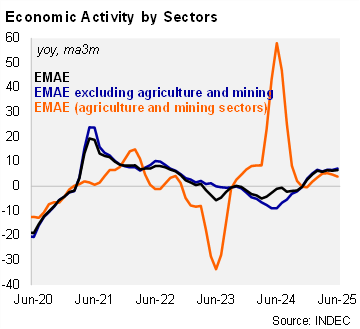

All sectors rose on an annual basis in 2Q25. Primary activities rose by 3.9% YoY during this period (compared to +5.0% YoY in 1Q25), while manufacturing expanded by 6.9% YoY in the same period (vs. a gain of 5.1% YoY in 1Q25). Services (including the commerce sector) rose by 5.0% YoY in the period (vs. 2.2% in 1Q25), likely supported by the recovery of real wages. Construction rose by 11.1% YoY in the period (from 6.2% YoY in 1Q25) due to a base effect amid the freezing of public works in the same period of 2024.

Our take: Our GDP growth for YE25 stands at 5.0%. A string of weaker-than-expected economic activity in recent months led us to revise our forecast down from 5.2%. Despite this, growth remains exceptional, reflecting progress in stabilizing and gradually liberalizing the economy over the last year. A positive outcome for the government in the midterm elections on October 26, 2025, would likely trigger an upswing to sentiment and investment. The monthly GDP proxy for July will be published on September 24.