2026/05/07 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

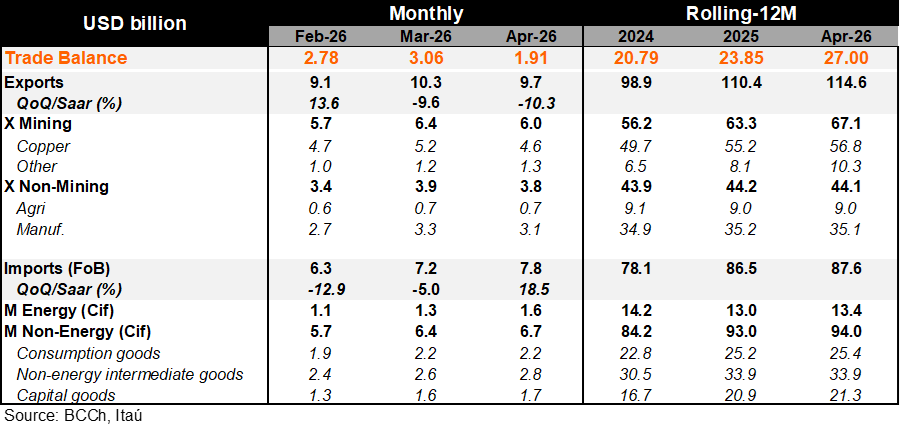

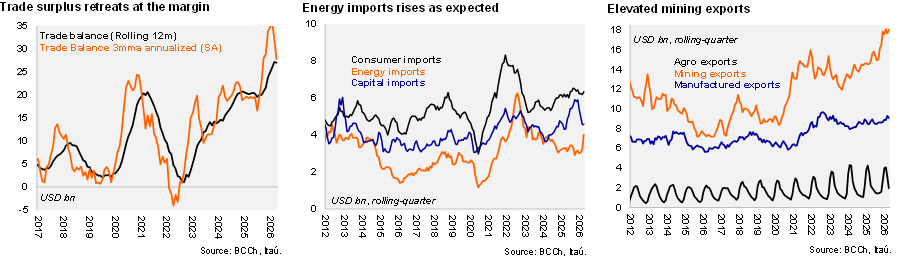

According to the Central Bank, the trade surplus reached USD 1.9 billion in April, below the market expectation of USD 2.5 billion, but closer to our forecast (USD 2.1 billion). As of result, the rolling 12-month trade surplus sits at USD 27 billion (USD 23.9 billion in 2025). During the month, total exports increased by 6.7% YoY (+18% in 1Q26). Mining exports rose by 15% (+24% in 1Q26), with gold and lithium exports making the largest positive contributions. In contrast, agricultural and industrial exports declined by 7.6% and 2.9%, respectively. On the import side, total imports grew by 11.8% YoY (+6% in 1Q26), with all categories contributing positively to the overall result. Consumer goods imports increased by 10.1%, capital goods imports rose by 9%, and energy imports surged by 31%, the latter being strongly driven by higher international oil prices.

Our take: The surge in international oil prices will limit record high terms-of trade levels present prior to the war. We expect the trade surplus to tick down to 6% of GDP (7% in 2025) as metal prices remain favorable. Overall, we see the current account deficit rising from 1.2% of GDP last year to a still low 1.7% this year.