At today's monthly monetary policy meeting, the central bank's Monetary Policy Committee kept the monetary policy rate at 6.00% for the fourteenth consecutive month. The decision was in line with our call and market expectations (according to the BCP's survey).

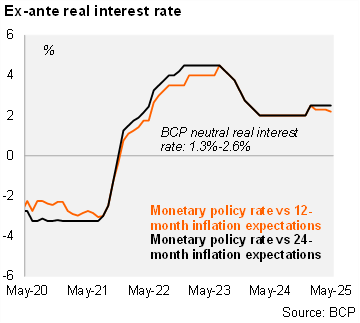

According to the statement, the committee reaffirmed its commitment to price stability and will continue to monitor internal and external developments to ensure the 3.5% inflation target is met. Moreover, despite a slight uptick in short-term inflation expectations, long-term expectations remain on target. Therefore, we estimate that the real ex-ante policy rate remains at 2.5% (using expectations for the monetary policy horizon), compared to the BCP's neutral real interest rate range of 1.3%-2.6%.

Regarding the global context, the BCP highlighted that the global financial market volatility declined due to easing trade tensions and fewer Fed rate cuts are now expected in 2025. Moreover, international oil prices fell due to improved supply outlooks. Soybean and wheat prices rose recently, while corn prices declined.

Our take: Our YE25 policy rate forecast stands at 6.0%. The policy rate is already at the upper bound of the BCP’s neutral range in real ex-ante terms. The next monthly monetary policy meeting is scheduled for June 24.