2025/12/09 | Diego Ciongo & Soledad Castagna

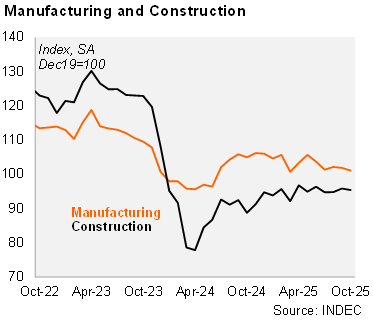

Manufacturing fell sequentially in October. The IPI manufacturing index decreased by 0.8% mom/sa in October, after falling by 0.2% in September. Thus, industry output fell by 1.8% qoq/sa in the quarter ended in October, following a 2.3% contraction in 3Q25. On an annual basis, manufacturing fell by 2.9% in October and by 2.6% in the quarter ended in that month. Only two of nine sectors grew on an annual basis in October.

Construction dropped in October. The construction index fell by 0.5% mom/sa in October, after growing 1.1% in the previous month. Moreover, construction remained unchanged (0.0% qoq/sa in the quarter ended in October (-1.0% qoq/sa in 3Q25). Construction activity increased by 8.0% yoy in October and by 5.1% yoy in the quarter ended in that month. Employment in the sector increased by 3.3% relative to September 2024 (figures have a one-month lag). According to a qualitative survey, 69% of those involved in private construction expect no changes in activity levels over the next three months. Meanwhile, 10.0% expect an increase and 21.0% anticipate a decline. Among companies primarily engaged in public works, 25% anticipate a decrease in activity levels during the next three months, while 60% expect no change and 15% expect an increase.

Our take: Despite weaker construction and manufacturing data in October, our 3.8% GDP growth forecast for 2025 has upside risks. The unusually large revision of the latest monthly GDP proxy (EMAE) reinforces our outlook, given the significant carryover. The national accounts data for 3Q25 to be published on December 16 will be key to confirm the rebound of activity after a temporary sequential drop in 2Q25. The GDP proxy for October will be published on December 22.